Why Google Pays Rent

The $30 billion SpaceX contract is the first public price of a layer that reorganized the AI stack — and the lens to read every announcement of the next six months

On Friday, June 5, SpaceX disclosed in a regulatory filing that Google will pay $920 million per month from October 2026 through June 2029 for access to approximately 110,000 NVIDIA GPUs hosted in SpaceX data centers, as reported by TechCrunch, confirmed by the New York Times, and covered by CNBC. The contract totals roughly $30 billion and lands four days before SpaceX’s IPO at a $1.75 trillion reference. Most weekend commentary treated the announcement as another recurring revenue line propping up the IPO multiple.

That reading misses the question. The right question is why Google — owner of the most mature TPU stack in the market, sitting on $80 billion in freshly raised equity for infrastructure capex, identified by TechCrunch’s own reporting as possibly the world’s largest single owner of AI compute — is paying $920 million a month to rent GPUs it could theoretically build itself.

The answer is that it can no longer build them. Not at the speed it needs. And that impossibility, hidden behind a contract that looks routine, is the clearest signal yet of a structural reorganization in the AI value chain. This essay delivers the framework — compute landlord — that explains, in a single move, the SpaceX-Google contract, Alphabet’s $80 billion raise, Apple’s licensing of Gemini, SpaceX’s acquisition of xAI in February, and the SOXX’s 10.4% selloff on Friday. They are moves of the same piece. Whoever sees the piece reads the next six months of announcements with analytical advantage over the rest of the market.

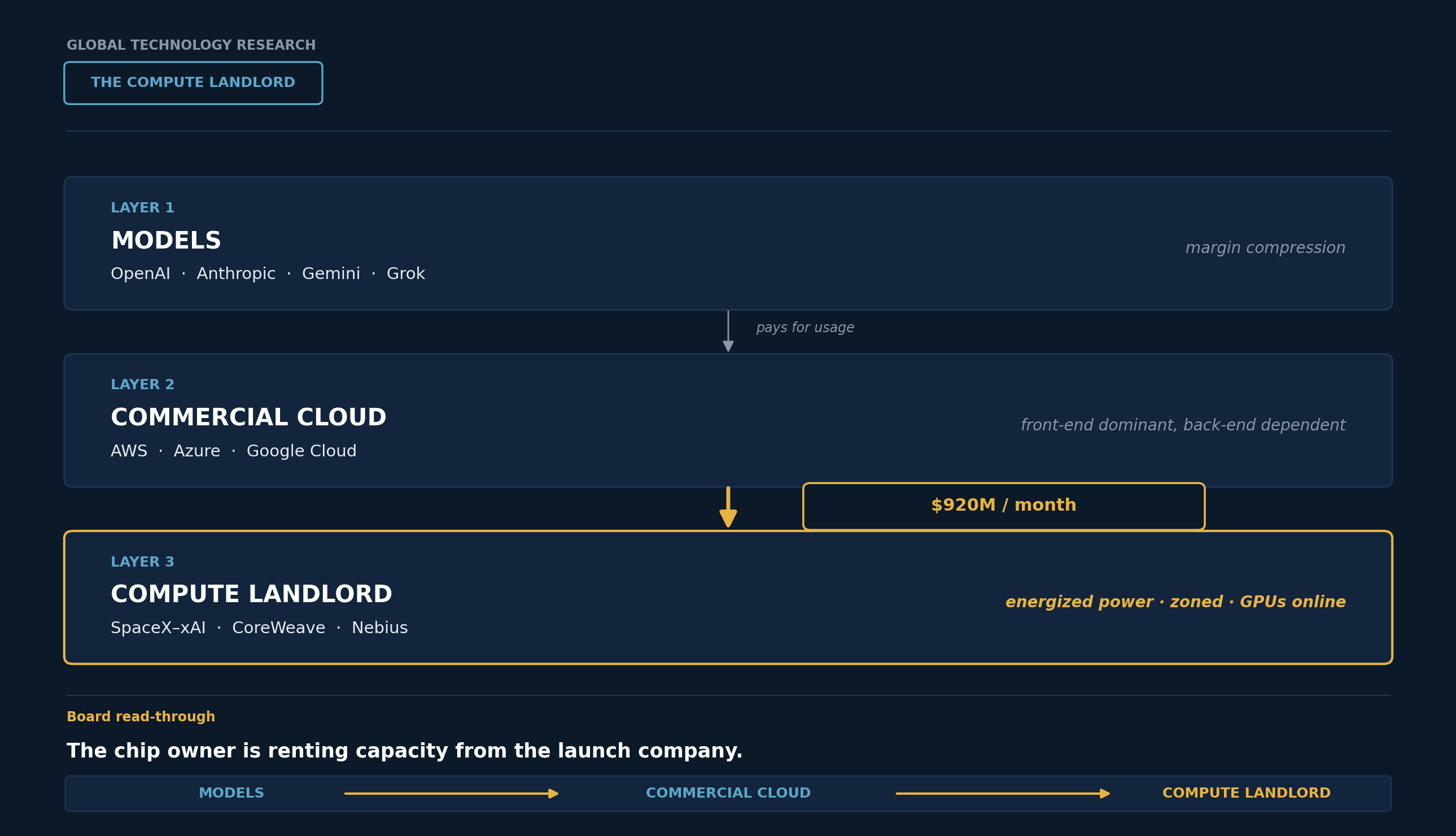

The three layers of the new stack

The AI value chain through 2024 had two layers that mattered: models at the top (OpenAI, Anthropic, Google DeepMind) and hyperscalers as unified infrastructure (AWS, Azure, GCP). The hyperscalers were simultaneously chip suppliers to their own cloud and capacity resellers to third parties. The physical layer — power, land, permitting, transmission — was treated as commodity, solved by capex.

In 2026 that premise broke. Three layers exist now, and the border between them defines bargaining power. The first is the model layer, where competition tightened and margin compressed. The second is the commercial cloud layer, where hyperscalers still own the front-end but lost autonomy at the back-end. The third is the new one, defined by three non-violable constraints: power available now, not in 2028; site approved, with no municipal moratorium or community litigation; and accelerators installed and energized, not merely ordered. This is the compute landlord layer.

SpaceX entered that third layer through a side door. By acquiring xAI in February, it inherited the Memphis Colossus — the cluster Elon Musk brought online in 122 days in 2024 using mobile natural-gas turbines, bypassing the conventional substation buildout. In October, part of that capacity becomes Google revenue. CNBC was explicit when framing the move: SpaceX now competes directly with CoreWeave and Nebius in the infrastructure leasing market — a category that barely existed twelve months ago.

The data from the other side of the market confirms this is not speculative. CoreWeave reported Q1 2026 revenue of $2.1 billion (+112% year-over-year), contracted backlog of $99.4 billion, 1 GW of active power and 3.5 GW contracted, with a new $21 billion commitment signed with Meta in March, per the company’s official investor release. In parallel, Broadcom announced on the Q2 call that FY26 AI revenue will land at $56 billion (+180%), FY27 above $100 billion, and that it is structuring a $35 billion SPV with Apollo and Blackstone to finance 20 GW of compute capacity for OpenAI and Anthropic through 2028, per analysis of the call by Market Musings. The quarterly guidance the market read as disappointment is, in fact, the opposite of the story told by the SOXX: physical compute supply is already sold far beyond what the chain can deliver.

On the opposite end, Anthropic has 1 GW of TPU contracted from Broadcom in 2026 and another 5 GW starting in 2027 — almost no proprietary capacity. It is a structural tenant with a confidential S-1 referenced at $965 billion, which means its entire valuation thesis depends on securing access to something it does not control.

Why the TPU owner is paying rent

The strongest objection comes from those who point out that Google has the most mature vertical stack in the world: in-house TPU since 2015, seven generations in production, deep partnership with TSMC. Why pay $920 million a month to access NVIDIA GPUs in someone else’s data centers?

Because owning the chip design, having infinite capital, and employing the best engineers in the world does not solve three physical problems. The substation needed to power 1 GW of new data center takes 36 to 60 months depending on the state. Municipal permitting collapsed under the last twelve months of community opposition — petitions exceeding 227,000 signatures in Nashville, shots fired at a councilman’s home in Indianapolis, a $15 billion project withdrawn in Utah. And the NVIDIA queue for H200 and Blackwell at volume is measured in quarters, not weeks.

SpaceX solved all three before the problem existed. Colossus was energized on gas. Zoning was filed under the “critical industrial infrastructure” classification, not “commercial data center.” The GPUs were already installed when SpaceX inherited xAI. Google is not renting GPUs. It is renting the time it lost building the wrong future.

The surface reading is that Google chose not to build. The structural reading is that Google can no longer build at the speed required to defend its position at the frontier, and the ready-capacity market today has exactly three suppliers at scale — CoreWeave, Nebius, and the newly formed SpaceX-xAI. That is the economic definition of a landlord oligopoly.

The lens the reader takes home

The practical utility of this essay starts here. Every time a meaningful AI announcement appears over the next six months, three questions separate landlords from tenants, and the answer dictates bargaining power.

The first is about energized power. How much capacity is physically operational today, with voltage on the bus, and not contracted for 2027? Whoever holds active gigawatts collects rent. Whoever holds contracted gigawatts pays rent.

The second is about the shape of expansion. Does the next MW come from a new substation that still needs approval, or from proprietary generation already locked in and outside the local utility queue? Whoever depends on the utility is at the back of the line. Whoever escaped the queue is already in production.

The third is about customer contracts. Are termination clauses short (the supplier didn’t need to concede, there is a waiting list) or long (the supplier conceded to close the deal)? The SpaceX-Google contract carries a 90-day cancellation window after December 2026, per the filing detailed by TechCrunch. Even the largest possible customer could not lock in tenor. That is landlord bargaining power visible in a single contract line.

Whoever answers “operational, proprietary, short” across all three is a landlord. Any combination involving “contracted, new, long” downgrades the position. The lens applies to any player that surfaces in coming pitches, calls, and announcements — Gulf neocloud, traditional hyperscaler, telco-AI joint venture. It applies, above all, to the uncomfortable question this rubric raises when turned on the current set of integrated hyperscalers: which of them, under these three questions, would discover that the vertical tower they bet the last decade on no longer puts them on the right side of the line?

Implications and the signal to track

For capital allocators, the SpaceX IPO is the first public test of what multiple the market will pay for a pure-play compute landlord. The signal to track is not SPCX’s specific opening price — it is whether that multiple, whatever it turns out to be, transfers to CoreWeave and Nebius in the following weeks. If it transfers, the frame has earned institutional validation and the landlord layer becomes a priceable asset class. If it does not, the market is still reading SpaceX as an exception, and the thesis has to wait for the Anthropic tape to be tested again. CoreWeave and Nebius already reacted positively to the SpaceX-Google announcement after Friday’s broader selloff, per CNBC’s coverage — a directional cue that leans toward the thesis.

For operators and AI founders, the due diligence question has migrated. It is no longer “who is your cloud provider” — it is “who is your compute landlord, for how long, with what termination clause.” Startups need to answer this in the next round of pitches the same way they answered the CFO question in 2021. Anyone without a clear answer is selling a model whose inference runs on third-party capacity that can be cut in 90 days.

And the directional signal to track over the next few quarters is qualitative, not numerical: the frequency with which new lease contracts appear between non-hyperscalers (sovereign funds, telcos, independent neoclouds) and the large compute consumers. The denser that mesh, the more consolidated the layer. If the direction reverses — if traditional hyperscalers start announcing proprietary buildouts at sufficient scale to no longer need to rent — the frame dissolves. But the current direction points the opposite way: Meta just closed an additional $21 billion with CoreWeave in March, a signal that even the hyperscaler with the most free capex chose not to build everything alone.

For a decade, the AI question was who would build the best model. The next decade asks who energized the best gigawatt before knowing it would matter. On Thursday, the first price prints.

— GTR Team

Great writeup. I think $TGEN is well positioned to take advantage of this. Reducing electrical consumption of around 30-35% using LNG chillers for cooling is going to be big in the coming years. While most are going to look at the companies opening up more GW's for use, there is some value in the companies making better use of currently available capacity.