The Prediction Economy

In eighteen months, betting on the future went from a crypto-Twitter curiosity to a $28-billion-a-month asset class. Here is what actually happened — and whether the prices mean anything.

Estimated reading time: ~9 min

For most of their existence, prediction markets were a footnote. A place where political obsessives and degenerate gamblers could put money on an election, watch a probability tick up and down, and feel briefly clairvoyant. Then, almost overnight, the footnote became the headline. Combined monthly trading volume across the two dominant platforms, Kalshi and Polymarket, climbed from under $5 billion in September 2025 to roughly $28 billion by May 2026. For comparison, Americans wagered about $14 billion a month through legal sportsbooks last year. The crowd-odds business is now twice that — and growing faster.

The trigger was regulatory, not technological. For three years Polymarket was effectively banned in the United States, forcing American traders onto VPNs and foreign wallets. In late 2025 the Commodity Futures Trading Commission, under a new chairman, withdrew its proposed restrictions and handed Polymarket a no-action letter — a green light to serve U.S. customers through a regulated intermediary. Kalshi, which had spent years securing the first CFTC license for an event-contract exchange, was already onshore and legal in all fifty states. The dam broke, and the capital that had been waiting on the sidelines poured in.

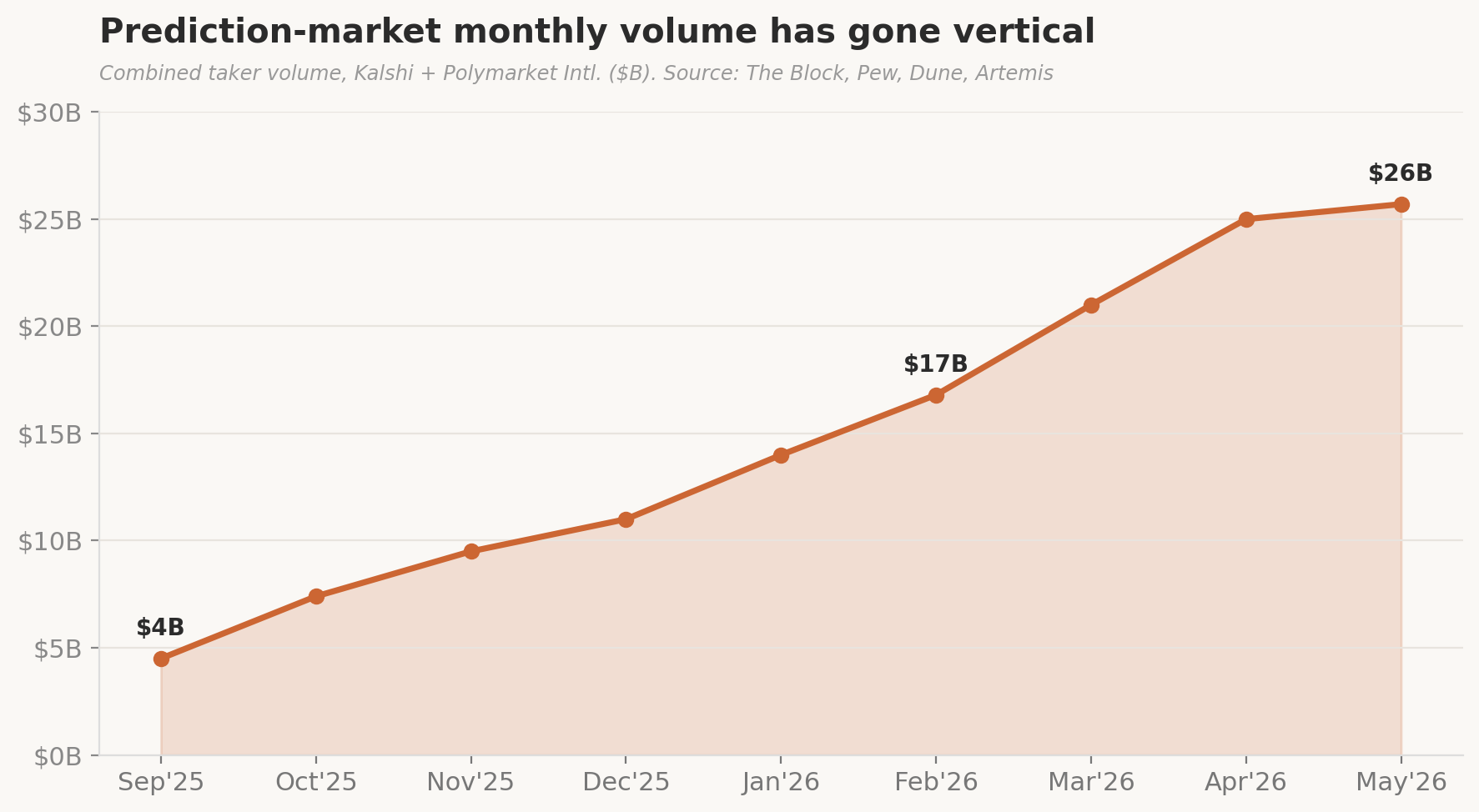

01 — The line went vertical

The growth chart is the kind that makes founders frame it and regulators nervous. Nothing about prediction markets was subtle in this stretch: a single Polymarket market on whether the U.S. would strike Iran drew $73 million in February alone, the largest geopolitical contract in the platform’s history. Polymarket set a single-day record of $425 million that same month — bigger than the frenzy of Election Day 2024. Kalshi crossed $1 billion in a single week of transactions.

Combined taker volume on Kalshi and Polymarket International. Volume roughly sextupled in eight months. Sources: The Block, Pew Research Center, Dune Analytics, Artemis.

What changed is not just the dollar figure but the character of the activity. Election betting was lumpy and seasonal — it spiked every four years and collapsed in between. Polymarket’s volume famously fell more than 80% in the months after the 2024 vote. The 2026 surge looks different: it is broad-based across sports, crypto, macroeconomics, and geopolitics, and it persists between marquee events. That is the signature of an asset class rather than a novelty. When Bitcoin dropped below $67,000 in early June and crypto markets saw their heaviest liquidations since February, traders piled into prediction contracts precisely because the downside is capped at the purchase price — no margin calls, no liquidation cascades. The product is starting to behave like infrastructure for hedging event risk, not just a casino for pundits.

Who is actually trading tells the same story. On-chain analysis segments the user base into clear cohorts: a large middle of active traders placing between a few dozen and a thousand bets, a smaller but heavy-hitting set of high-frequency market makers, and a steady drip of new entrants. The number of wallets interacting with Polymarket more than tripled in six months. This is no longer a few thousand election obsessives; it is a maturing market microstructure, with the same maker-taker dynamics and liquidity-provider economics you would find on any exchange. That maturation is exactly what lets the platforms argue they are financial venues rather than gambling parlors — a distinction worth billions in valuation and, as we will see, an open legal question.

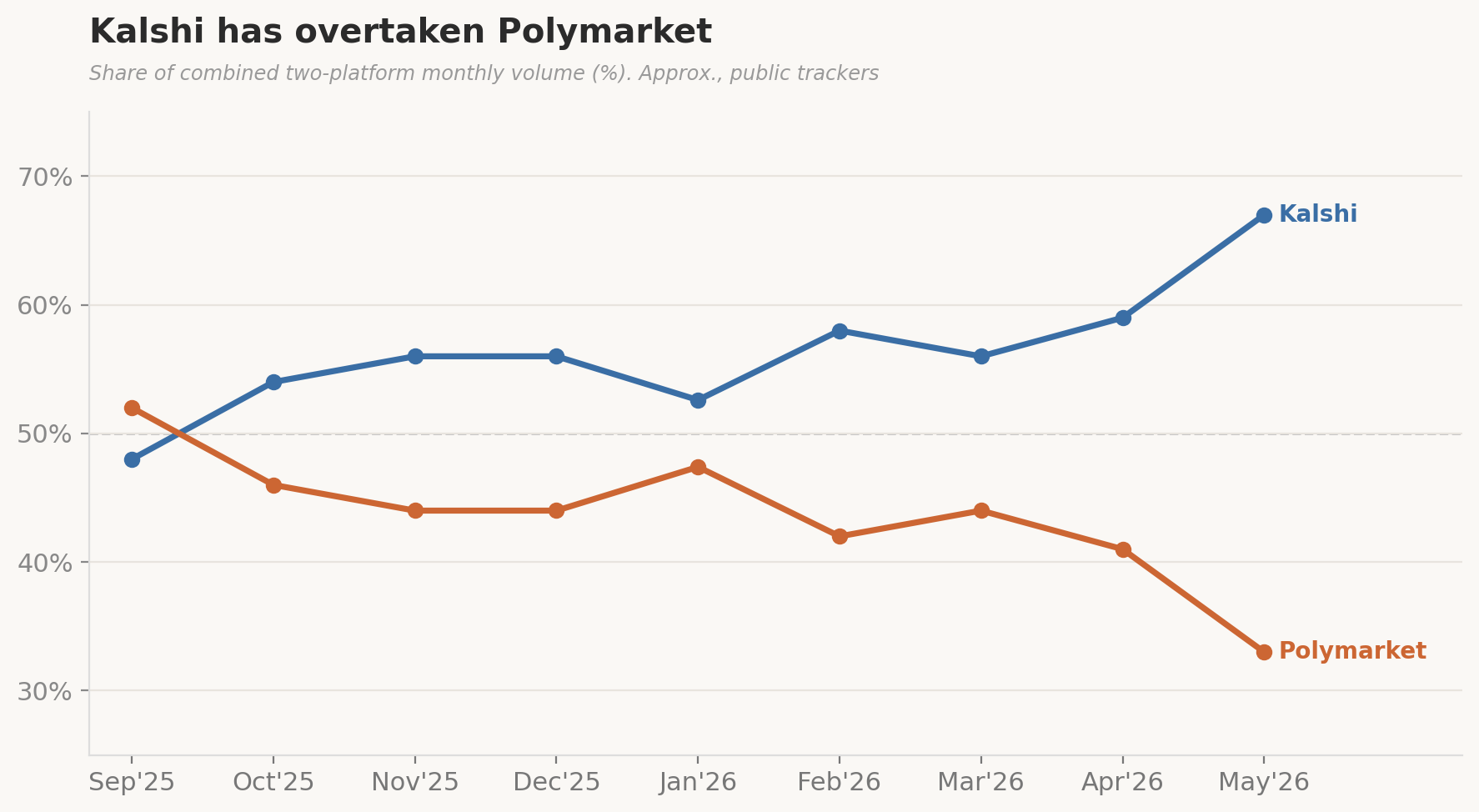

02 — A two-horse race, and the lead changed hands

For years, Polymarket was the name everyone knew. It was the platform that called the 2024 election while pollsters hedged, the one Elon Musk amplified, the one that turned “the odds” into a media artifact cited on cable news. But the regulated rival quietly overtook it. Through the second half of 2025 and into 2026, Kalshi pulled ahead in raw volume and kept widening the gap.

Approximate share of combined two-platform monthly volume. Kalshi crossed Polymarket in late 2025 and reached roughly two-thirds by May 2026. Sources: Dune, The Block, DeFi Rate, Artemis.

The crossover is a story about what each platform is. Kalshi is a CFTC-regulated exchange that charges fees from launch, operates legally onshore, and has leaned hard into sports — which now accounts for roughly 80% of its volume — plus macroeconomic and political contracts that institutions can actually touch. It signed the NHL as its first league licensing partner, secured the right to offer margin trading to institutional clients, and even launched in Brazil. Polymarket, by contrast, is a non-custodial protocol built on Polygon: more global, more crypto-native, dominant in politics and fast-moving geopolitical markets, but slower to monetize. It only rolled out broad fees on March 30, 2026, and its U.S. arm remains invite-only and limited to sports, walling American users off from the geopolitics and crypto markets that drive its international volume.