Return on Token

Why ROE is about to mislead everyone

Compute economics · the unit of production is changing · ~12 min read

Every era of business has had a denominator.

The metric that mattered was never just the profit on top. It was always profit divided by the scarce thing underneath — the input that was hard to get, expensive to hold, and dangerous to waste.

For a century, that denominator was capital.

Return on Investment. Return on Equity. Return on Invested Capital. Different formulas, one shared assumption: money is the scarce input, and the job of a great company is to wring the most output from each unit of it.

That assumption is now quietly breaking.

In an AI-native business, the marginal unit of production is no longer a dollar of capital or an hour of labor. It is a token.

And the moment your scarce input changes, every ratio built on the old one starts to lie to you.

That is the surface read: a new buzzword, another three-letter metric to roll your eyes at.

The deeper read is more uncomfortable:

ROE is about to flatter exactly the wrong companies, and punish exactly the right ones, for the next five years.

The denominator keeps moving

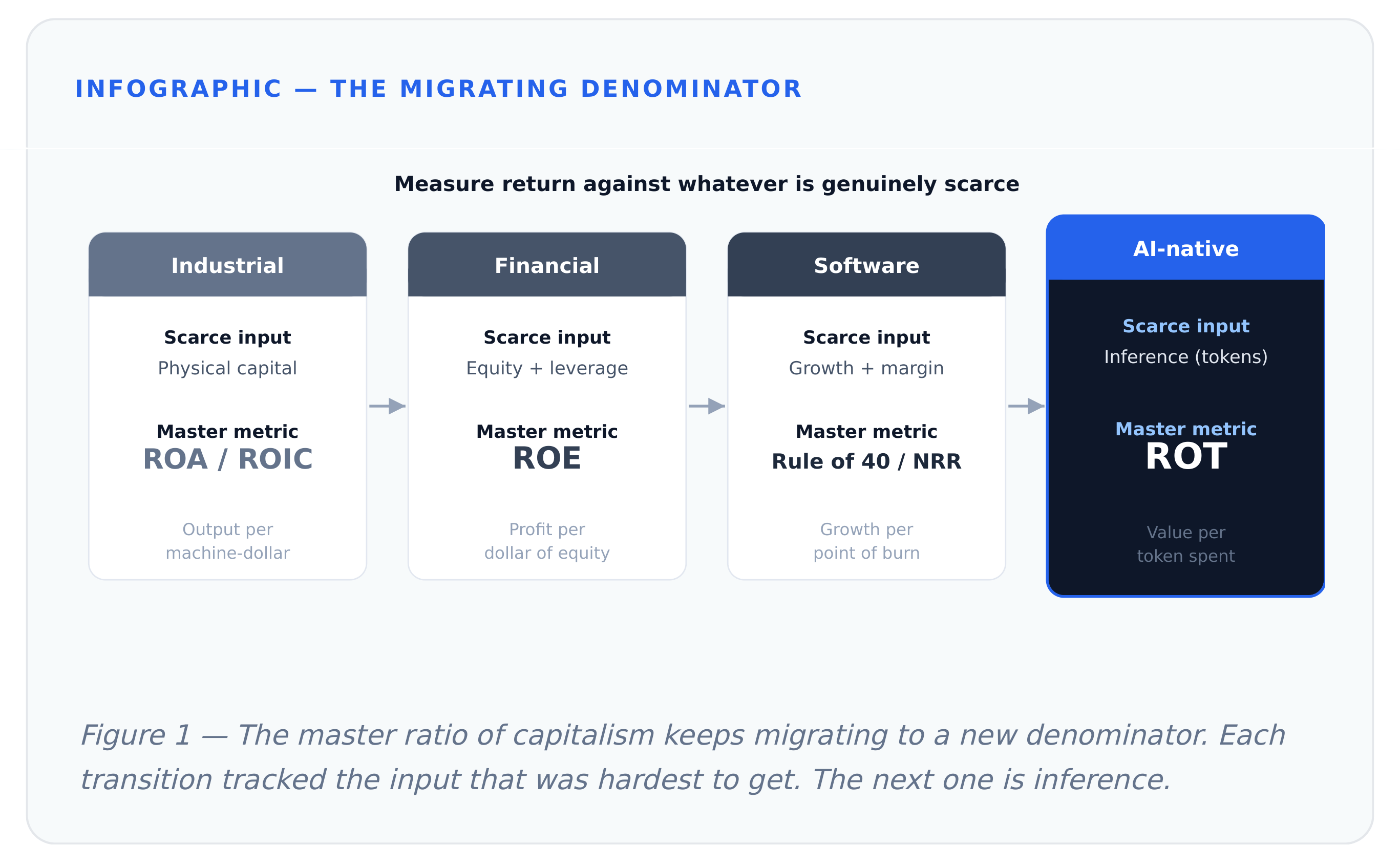

Look at how the master ratio of capitalism has migrated.

In the industrial economy, the binding constraint was physical capital — factories, machines, inventory. So we measured Return on Assets and Return on Invested Capital. The winner was whoever turned steel and working capital into product most efficiently.

In the financial economy, the binding constraint became shareholder equity and the leverage stacked on top of it. So Return on Equity became the king metric — the number that governs bank valuations, buyback programs, and executive comp to this day.

In the software economy, capital nearly stopped being the constraint at all. A SaaS company could serve a million more users for almost nothing. So the market stopped paying for capital efficiency and started paying for growth and gross margin — the now-familiar Rule of 40, net revenue retention, CAC payback.

Each shift followed the same logic: measure return against whatever is genuinely scarce.

In the AI-native economy, a new thing is scarce. Not capital — there is a tidal wave of it. Not code — models write it now. What is scarce, metered, and directly convertible into output is inference. Tokens in, tokens out. Intelligence by the unit.

Figure 1 — The master ratio of capitalism keeps migrating to a new denominator. Each transition tracked the input that was hardest to get. The next one is inference.

What Return on Token actually is

Strip the jargon and ROT is simple:

Return on Token = economic value produced ÷ tokens consumed to produce it.

It is the gross margin of intelligence. How much real-world output — revenue, resolved tickets, closed deals, lines of shipped code, diagnoses, underwriting decisions — you extract from each unit of inference you pay for.

Two forces make this the metric of the decade, and they pull in opposite directions.

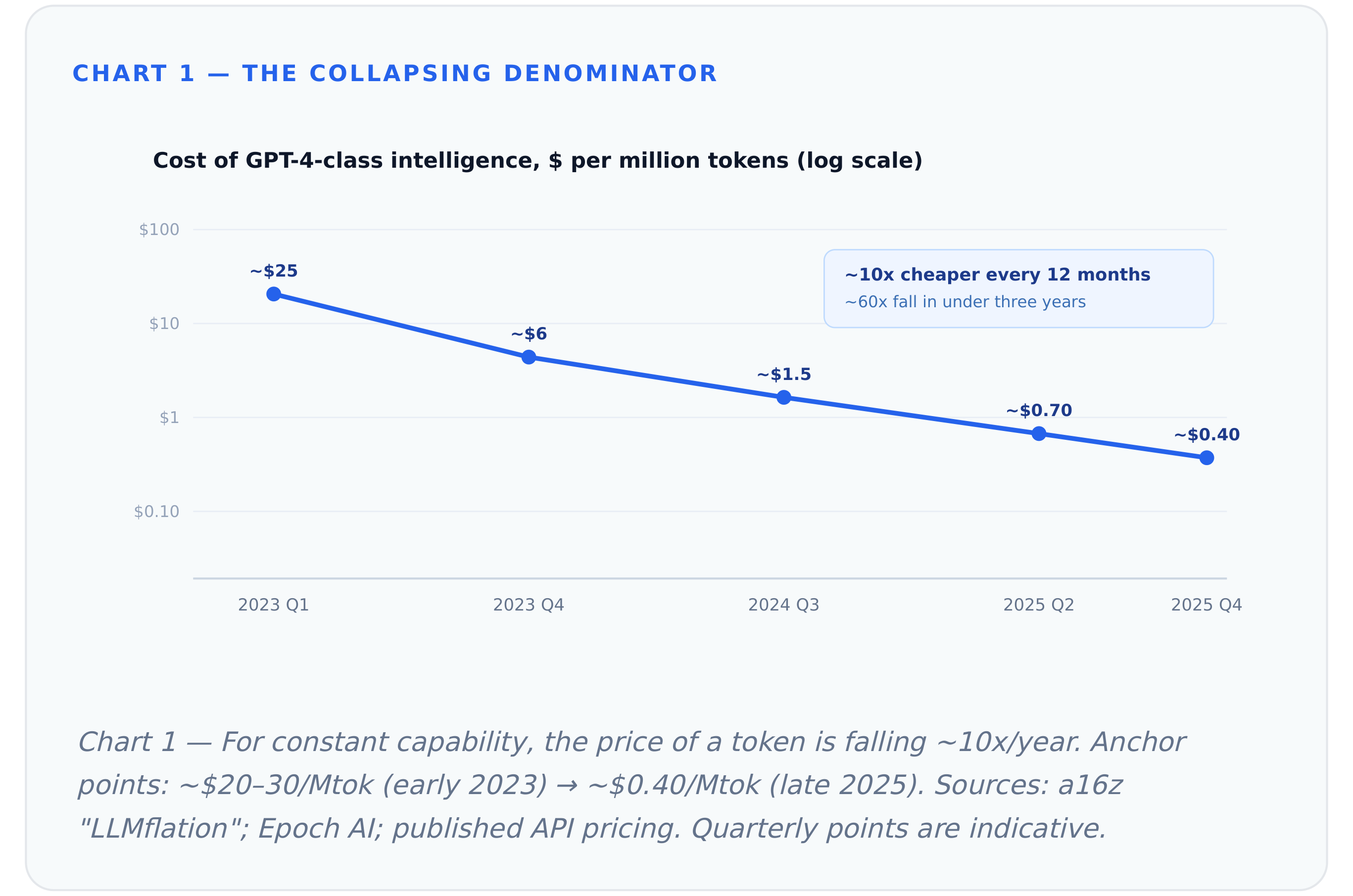

The denominator is collapsing. The cost of a token is in freefall. For a constant level of capability, inference cost has fallen roughly 10x per year — faster than compute fell during the PC era or bandwidth during the dotcom boom. GPT-4-class quality cost around $20–30 per million tokens in early 2023; by late 2025 it was about $0.40. Epoch AI clocks the rate accelerating past 200x per year in some segments after competition intensified.

The numerator is exploding. Tokens are no longer used only to autocomplete a sentence. They run agents, draft contracts, triage patients, write and review their own code. The same token that cost more and did less in 2023 now costs almost nothing and can carry a unit of genuine work.

When your cost-per-unit-of-intelligence falls 10x a year while the work each unit can do rises, the binding question for any business stops being “how much capital did you deploy?” and becomes “how much value do you extract per token?“

That ratio is ROT. And it is invisible on every financial statement filed today.

Chart 1 — For constant capability, the price of a token is falling ~10x/year. Anchor points: ~$20–30/Mtok (early 2023) → ~$0.40/Mtok (late 2025). Sources: a16z “LLMflation”; Epoch AI; published API pricing. Quarterly points are indicative.

Why ROE is about to lie

Here is the mechanical problem.

Return on Equity is net income over shareholder equity. It rewards a company for producing profit on a small equity base. For a hundred years that was a feature: it forced discipline on how much capital you tied up.

Now watch what AI does to both halves of that fraction.

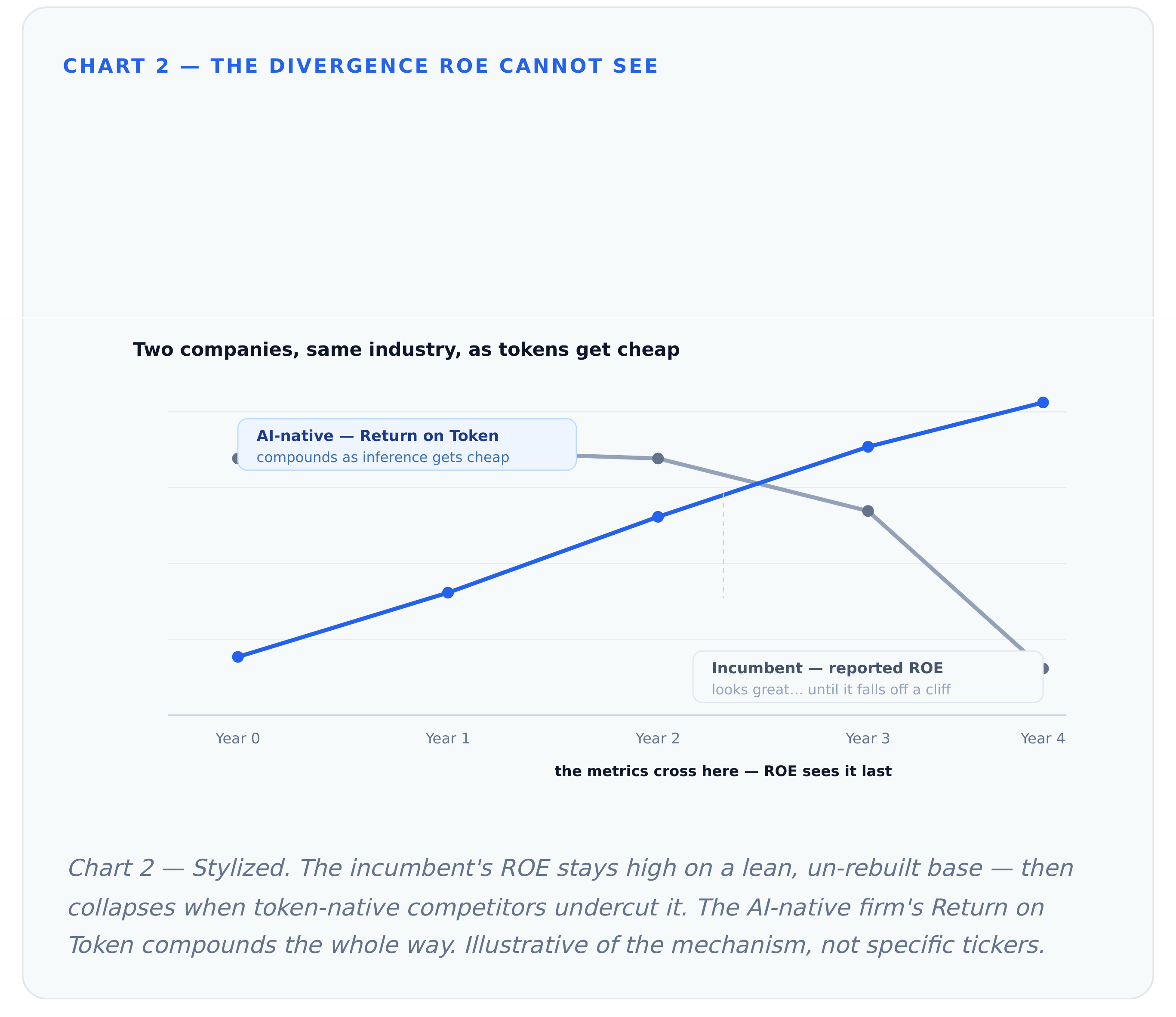

The companies generating the most genuine economic leverage from AI are doing something ROE cannot see: they are spending heavily on inference and R&D to build token-efficient systems — evaluation loops, agent harnesses, fine-tuned vertical models — that throw off enormous output per token. Much of that spend hits the income statement as cost, depressing near-term net income. Their ROE looks worse while their real engine gets better.

Meanwhile, the companies most exposed to disruption can post beautiful ROE right up until the moment they break. A legacy business process outsourcer, a high-margin call-center operator, a manual underwriting shop — each can show pristine returns on a lean equity base, precisely because they have not spent to rebuild on tokens. ROE flatters them for their inaction.

ROE measures how little capital you used. ROT measures how much intelligence you converted. In a world where intelligence is the scarce input, the first number can be high while the business is quietly dying.

This is not hypothetical. It is the same trap that caught newspapers around 2005. Print classified businesses showed gorgeous margins and returns — the year before Craigslist and Google hollowed them out. The accounting metric was healthy because it was measuring the wrong denominator. The scarce input had already moved from “column inches” to “attention,” and the income statement was the last to know.

We are about to run that experiment again, economy-wide, with capital as the obsolete denominator and tokens as the new one.