Has SOX peaked out? – A personal view on the current semiconductor cycle

Previous articles on this blog have discussed individual stocks in the semiconductor industry. Nevertheless, due to recent market volatility, some readers have suggested to me that, as an experienced investor in the semiconductor sector, I could share my views on the current semiconductor industry cycle. Other readers have also asked me for interpretation of the two semiconductor cycle charts I posted in my Notes earlier. Therefore, today I will briefly discuss my views on the semiconductor cycle.

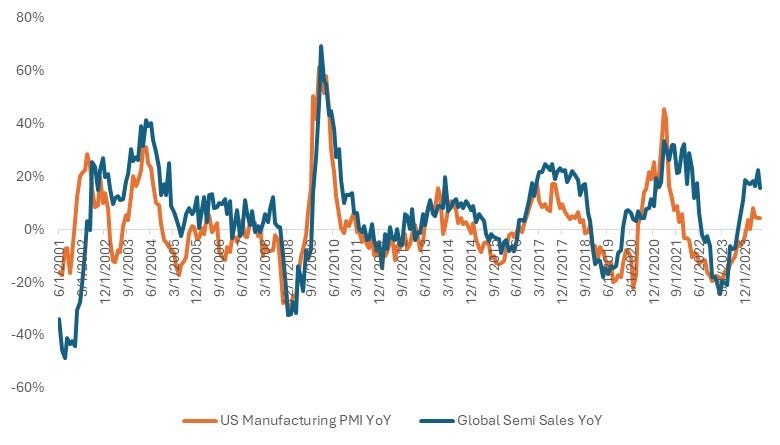

Let me get straight to the point first: Based on my experience of over a decade investing in the semiconductor industry, the most relevant indicator for the semiconductor cycle is the US Manufacturing PMI YoY growth (see the chart below). Historically, whenever the US Manufacturing PMI YoY growth rate drops to around 0% level, it triggers a significant decline in the SOX (Philadelphia Semiconductor Index), marking the end of a semiconductor cycle.

Let's play a game here: Suppose I were a novice investor with no knowledge of semiconductor industry. Could I use a simple method of tracking monthly US Manufacturing PMI data to decide when to exit the SOX?

Let’s review the three previous semiconductor cycles: The last SOX peak was in December 2021. Since US Manufacturing PMI data is released at the beginning of the following month, in December 2021 we could only observe the US Manufacturing PMI YoY growth rate for November 2021, which was 6%. Similarly, the previous SOX peak was in September 2018, when the US Manufacturing PMI YoY growth rate was 4%. The peak before that was in June 2015, when the US Manufacturing PMI YoY growth rate was -5%. This suggests a doable strategy that when the US Manufacturing PMI YoY growth rate falls to around ±5% level, taking profits on SOX might allow you to exit at the peak.

Interestingly, examining the three semiconductor cycles over the past decade reveals that the market has continually learned and evolved: In 2015, the market seemed to lack a common understanding of the semiconductor cycle's close correlation with the US PMI, only realizing the semiconductor cycle had peaked by June when the US Manufacturing PMI YoY growth rate had turned negative. By 2018, the market had learned from previous experience and started reacting when the US Manufacturing PMI YoY growth rate dropped to 4%. By the end of 2021, the market responded even earlier, starting to sell off SOX when the US Manufacturing PMI YoY growth rate dropped to 6%. At that time, the fundamentals of semiconductor companies were still healthy (SOX peaked on the first trading day of January 2022, while the fundamentals of semiconductor companies did not start deteriorating until early March, compared to October 2018 when the SOX sell-off was triggered by disappointing third-quarter earnings).

Recently, Mark Lipacis (former chief semiconductor analyst at Jefferies) suggested that this current SOX decline is merely a mid-cycle correction for the semiconductor industry. His core argument is that whenever global semiconductor sales YoY growth rate peaks, SOX experiences a significant pullback. However, this should be a golden buying opportunity because SOX will rise again thereafter, driven by positive earnings revisions of semiconductor companies. His mid-cycle correction theory did make sense historically, but Mark overlooks a point that differentiates this current SOX "mid-cycle correction" from past ones: In the past, when the global semiconductor sales YoY growth rate peaked, the US Manufacturing PMI YoY growth rate was around 20% or higher. This time, it is only about 5%.

In fact, from the perspective of investment psychology, it is not difficult to understand why SOX could continue to rise after a mid-cycle correction in the past. Semiconductor companies are mostly positioned upstream in the manufacturing supply chain. Thus, it takes several months for the deterioration in the Manufacturing PMI YoY to impact semiconductor companies’ earnings (each layer of the supply chain companies build up inventory, hence extending the transmission process). Historically, when the global semiconductor sales YoY growth rate peaks, it is usually still very high, often above 20%, and the earnings growth of individual companies will be even higher (due to operating leverage). Therefore, from an investor's perspective, seeing semiconductor companies’ earnings growth drop from 30+% to 20+% might not signal that the semiconductor cycle has peaked out. It is often interpreted as a high base effect instead, which is why SOX could still reach new highs after a mid-cycle correction. Only when companies’ earnings growth falls from ~20% to ~10% or even single-digit % do investors begin to seriously worry about the downturn in the semiconductor cycle, leading to a major drop of SOX. If readers carefully examine the global semiconductor sales YoY chart shown above, you will find that SOX could still rise when YoY growth rate is just peaking but still maintained at relatively high levels. SOX truly collapses only when global semiconductor sales YoY growth rate starts to accelerate downward.

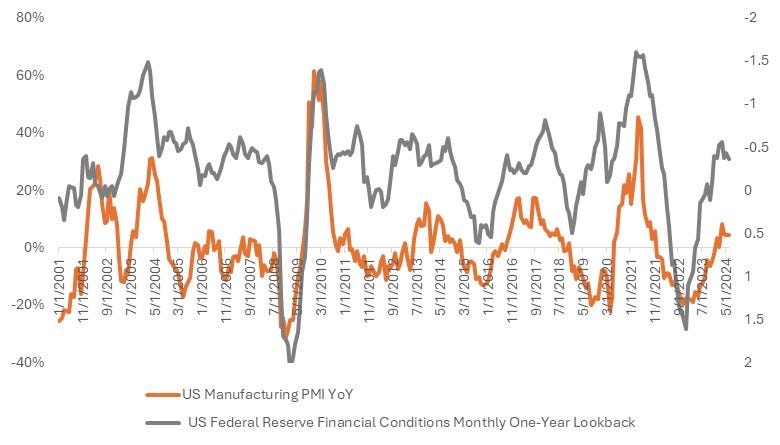

As mentioned earlier, when the global semiconductor sales YoY growth rate peaked in the past cycles, the US Manufacturing PMI YoY growth rate was around 20% or higher. Therefore, when the Manufacturing PMI YoY starts to decelerate from a high level, global semiconductor sales YoY growth rate can remain high for some time (due to inventory build in the supply chain) before dropping to near 0% level, allowing SOX to continue rising for several months after a mid-cycle correction. However, as shown in the chart above, this time when the global semiconductor sales YoY growth rate peaked, the US Manufacturing PMI YoY growth rate was only around 5%, with the most recent July PMI YoY growth rate dropping to merely 0.6%. Compounding the situation, the US financial conditions index, as a leading indicator of US Manufacturing PMI YoY, has also recently shown signs of peaking (see the chart below). Therefore, if this trend continues, the US Manufacturing PMI YoY growth rate might fall to 0 or even negative levels in the coming months. Under such weak manufacturing conditions, it remains a question mark whether global semiconductor sales YoY growth rate will be able to maintain at high level for several months after peaking. Historically, when the US Manufacturing PMI YoY growth rate falls below 0, global semiconductor sales YoY growth has tended to accelerate its decline trajectory.

In summary, I am more cautious about the SOX rebound after this correction and would suggest monitoring the US financial conditions in the next few months for further judgment. Unfortunately, it seems that only a Fed rate cut starting in September could potentially rescue the US Manufacturing PMI, and in turn, save this semiconductor cycle (Fed is behind the curve?). However, how long it will take for a September rate cut to positively impact the manufacturing sector is also uncertain, as Michael Hartnett (BAML chief strategist) wrote in his recent report: “People underestimate how much lower rates may need to go to stimulate a weak economy no longer juiced by government spending”……